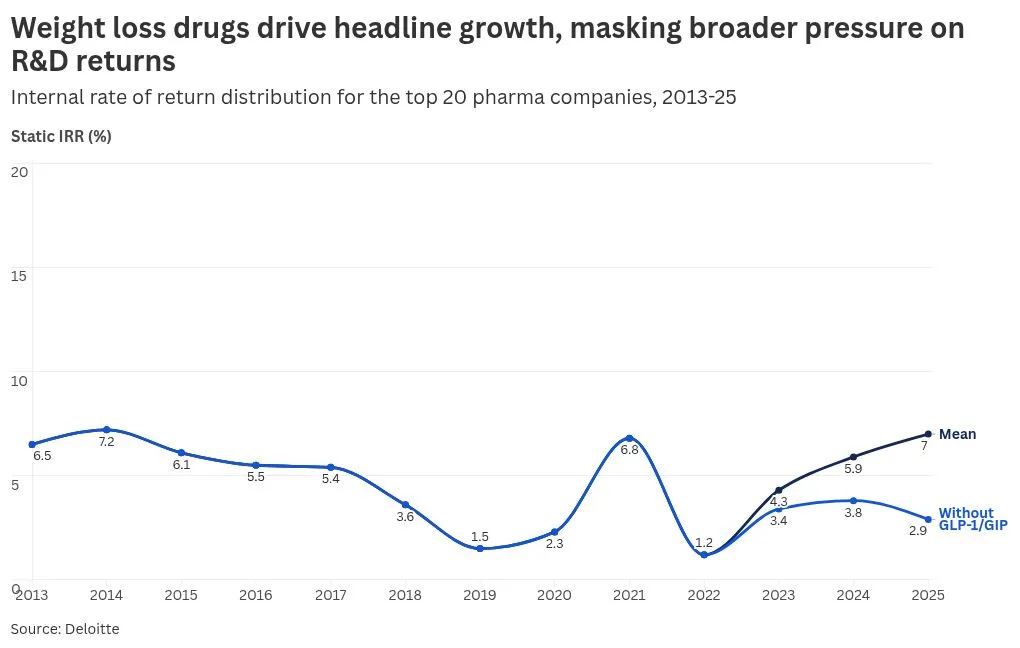

Pharmaceutical research and development returns at the world's top 20 companies reached 7%, their highest in years, driven by strong demand for weight loss and diabetes drugs like Wegovy and Zepbound, according to a Deloitte report published May 4 [1].

For the first time since 2010, obesity treatments have eclipsed oncology as the largest contributor to late-stage pipeline value in pharma. Drugs targeting obesity and diabetes now account for an estimated 38% of all projected commercial inflows from the 2025 late-stage pipeline [1]. Obesity-related assets represent about 25% of total forecast sales, while oncology’s share has slipped to 20% [1].

Excluding GLP-1 and GIP obesity and diabetes assets, the industry’s rate of return on R&D would fall sharply to 2.9%, down from 3.8% in 2024 [1]. This shows how heavily the sector is relying on these therapeutic areas.

The late-stage pipeline includes 54 mega-blockbuster drug indications—only 9% of the cohort—that are projected to generate roughly 70% of total risk-adjusted peak sales [1]. This concentration fuels what Deloitte calls a "bubble effect," increasing the pharma sector’s exposure to shocks in obesity and diabetes markets.

Hanno Ronte, Life Sciences and Healthcare Partner at Deloitte, said simply: "It is a bubble, because so much is concentrated" [1].

The Deloitte report highlights the growing risks to pharma despite headline R&D growth, as companies heavily weight pipelines on a small set of obesity and diabetes assets.

The report was released yesterday, May 4, underscoring the sector’s evolving focus and risk profile [1].