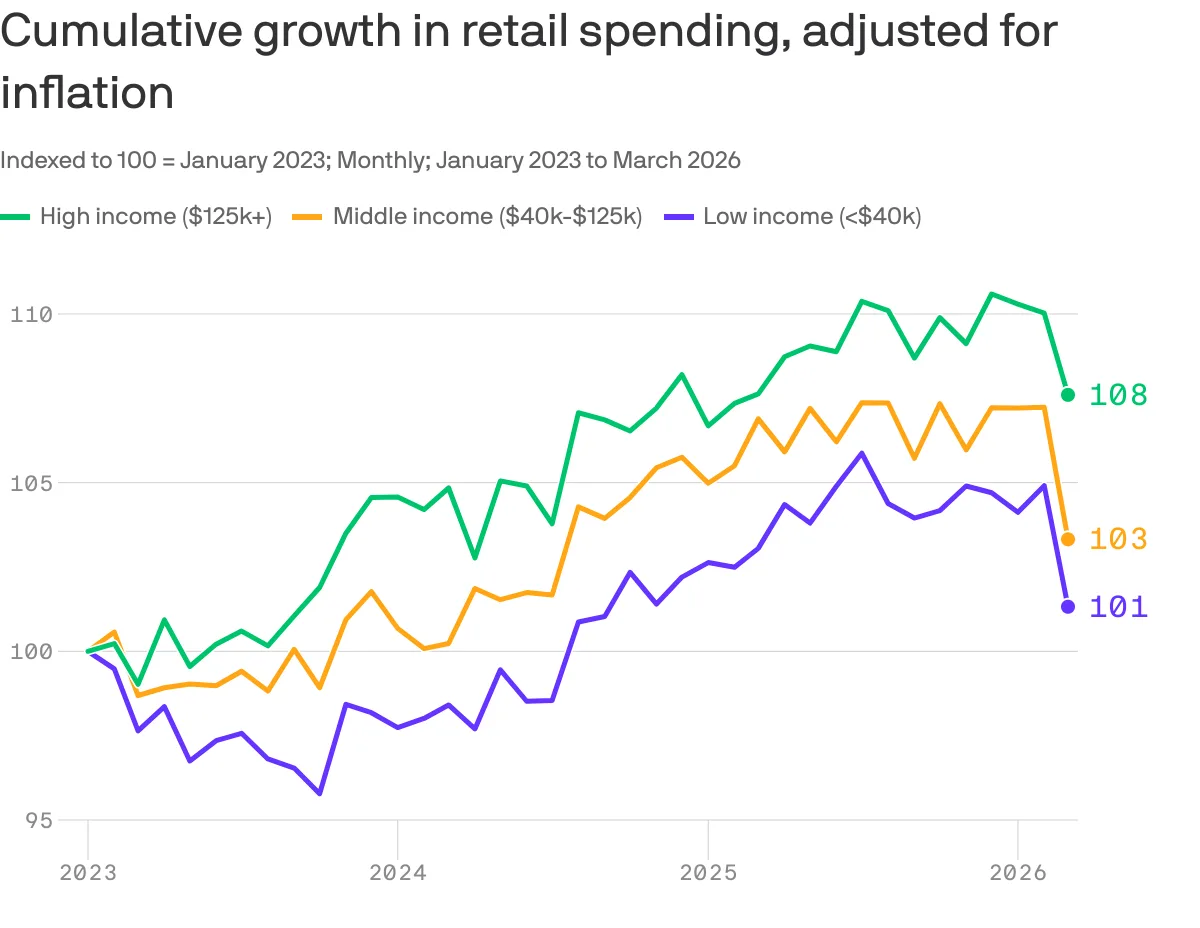

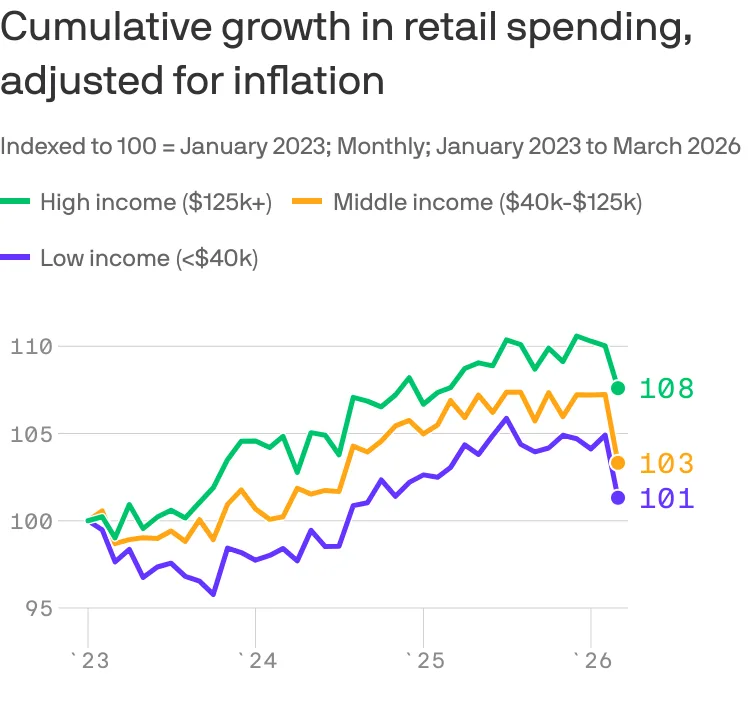

Since January 2023, real retail spending growth in the US has varied significantly by income group, according to data released by the New York Fed through March 2026 [1]. High-income households earning more than $125,000 annually saw the strongest gains, with cumulative real spending growth of about 7.6% over this period [1]. Middle-income households reported roughly 3% growth, while low-income households earning under $40,000 increased spending by just over 1% [1].

Before the COVID-19 pandemic, lower-income households led spending growth compared to wealthier households, but this trend reversed in 2023 after federal pandemic relief programs expired [1]. The recent rise in retail spending has been largely driven by the highest earners, creating a clear K-shaped spending pattern that the New York Fed says reflects increased economic inequality [1].

In most recent months, real spending growth has turned negative across all income groups, though the gap between high- and low-income households remains prominent [1]. New York Fed researchers noted that wage growth differences do not fully explain these spending trends. Instead, rising wealth and inflation are more important factors shaping the divergence [1].

The net worth of the top 1% of households has increased by more than 25% in real terms since 2023, mostly due to gains in financial assets, while the middle 40% of households have seen less than a 10% increase in net worth [1]. The study emphasized the risks of economic reliance on a single segment, stating, "Reliance on a single segment of the economy has important implications for spending growth and its fragility, as well as for economic vulnerability and policy" [1].