The Japanese yen slid approximately 1% this week, trading near 158.47 against the US dollar by May 15, marking its largest weekly loss in two months despite massive government intervention efforts [1, 2, 3].

Between April 30 and May 6, during Japan’s Golden Week holidays, authorities intervened in currency markets by purchasing an estimated 10 trillion yen—about US$63 billion—to support the yen and curb its decline [1, 4, 3]. The interventions initially boosted the currency but the yen has since retraced more than half of those gains.

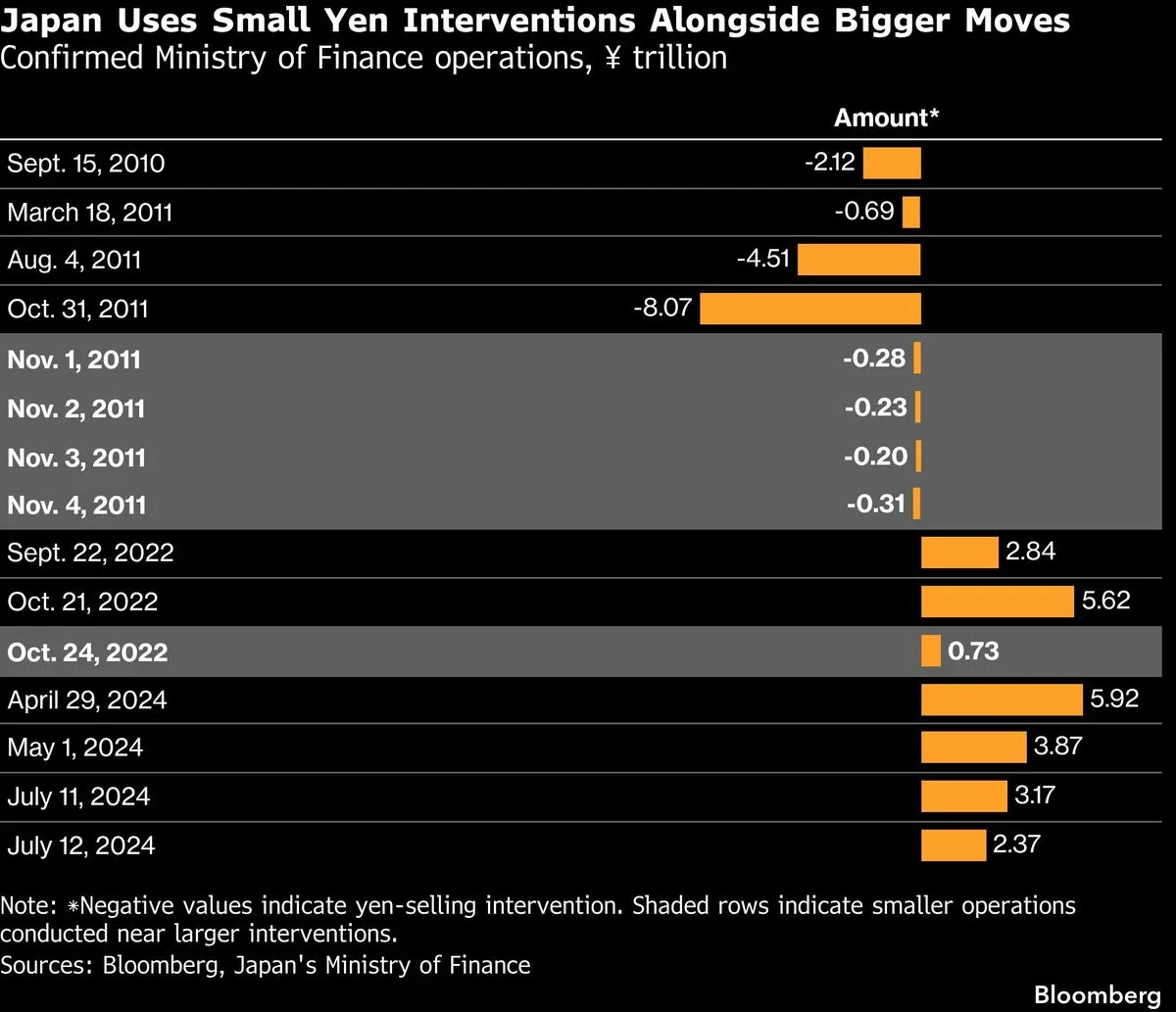

Multiple sharp intraday yen rises followed by quick reversals have occurred, including a 0.2% spike on May 8 and a 0.5% spike on May 12, leading some traders to speculate these moves reflect smaller-scale or less visible interventions by Japanese officials acting as “warning shots” to discourage further yen depreciation [4, 5]. Gareth Berry, strategist at Macquarie Group Ltd, said, "The Ministry of Finance is uncomfortable with dollar-yen above 160 and wants to discourage another test of that level. These proactive nudges and warning shots—even before 160 is reached—point in this direction" [4].

Several factors are putting downward pressure on the yen, including elevated oil prices, broad US dollar strength, ongoing conflict in Iran, and a wide interest rate gap between Japan and the US [1, 3]. The Bank of Japan (BOJ) is not expected to raise interest rates before mid-June, though markets currently price a 77% chance of a hike then [1, 3].

BOJ board member Kazuyuki Masu advocated for an early rate increase if economic stability holds, citing the risk of sustained inflation from the Iran war. He said, "Interest rates should be increased as soon as possible, provided there is no indication of the economy running into trouble" [1, 3].

Vincent Chung, portfolio manager at T Rowe Price, noted that "the effectiveness of further intervention will likely be determined by whether there is dollar weakness as well. An accelerated hiking cycle for BOJ would also help close the interest rate differential gap" [1].

Market participants remain cautious, holding expectations of possible further intervention, which have so far prevented the yen from falling beyond 160 per dollar [1, 4, 3]. The coming weeks will reveal whether the BOJ moves ahead with rate hikes and whether the US dollar weakens, key factors for the yen’s direction.

The next major event for the yen will be the Bank of Japan’s interest rate decision scheduled for mid-June, when markets await a possible policy shift that could alter currency trends [1, 3].