India raised tariffs on gold and silver imports from 6% to about 15%, combining a 10% basic customs duty with a 5% agriculture infrastructure and development levy, effective May 13, 2026 [1, 2, 3, 4, 5]. The government aims to curb bullion purchases and support the rupee, which hit an all-time low amid the Middle East war and rising energy prices [1, 2, 4, 5].

India also tightened silver import rules starting on May 16. Imports now require licenses from the Directorate General of Foreign Trade, effectively limiting most silver shipments and reducing import volumes [6, 3]. A government order that took effect May 17 further curbed silver supply by restricting imports of most forms, tightening domestic availability [3].

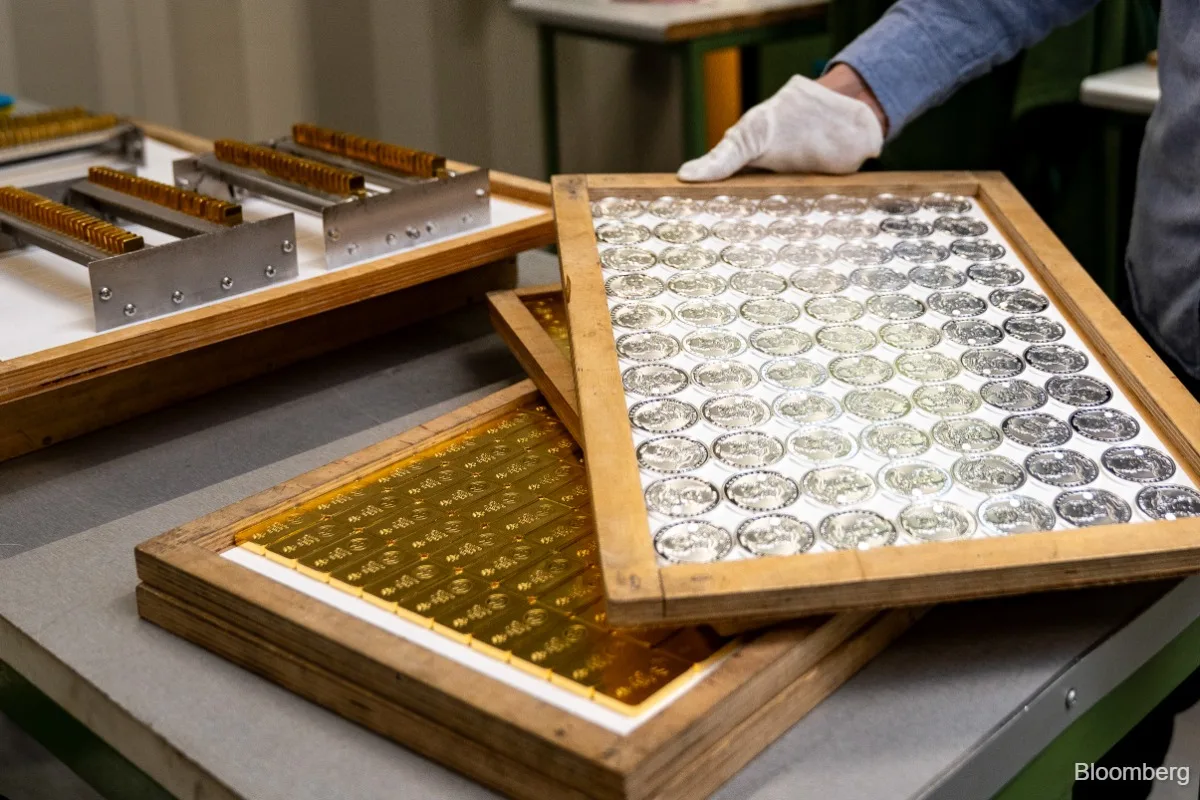

The tariff increase and import restrictions come after India spent a record $84 billion on gold and silver imports in the fiscal year ending March 2026, nearly triple the $35.5 billion spent a decade earlier [7]. Gold and silver accounted for nearly 11% of India's total imports by value last fiscal year, contributing to a merchandise trade deficit exceeding $330 billion [5].

Monthly average gold imports rose sharply in recent months, from 53 tonnes in 2025 to 83 tonnes in January-February 2026 due to strong investment demand [5]. India imported about 710 metric tons of gold last year and remains the world's second-largest gold consumer and largest silver consumer [7, 4, 5]. Silver imports jumped 157% year-on-year in April 2026 to $411 million, driven by record inflows into silver ETFs [3]. Most silver is imported from the UAE, UK, and China, for use in jewelry, coins, bars, and industry [3].

Domestic gold prices have yet to fully reflect the additional costs from higher tariffs, but imports have slowed substantially [1]. Chirag Thakkar, CEO of Amrapali Group Gujarat, said, "This move will reduce imports and tighten supplies in the local market. Silver had been trading at a discount after the government raised import duties, but it is likely to start trading at a premium in the coming weeks." [3]

Despite tariff hikes and price gains, demand for gold remains resilient due to its cultural significance and use as a financial hedge and loan collateral [7]. Vishrut Rana, Asia-Pacific economist at S&P Global Ratings, said lower gold imports can help reduce current account outflows, "But energy costs are still front and center, and while these are elevated, we expect pressure on the rupee will persist." [5] Trinh Nguyen, senior economist at Natixis, added, "India is backtracking on liberalization of the market, which investors like about India." [5]

India has also urged citizens to curb gold purchases and non-essential foreign travel to support the currency amid economic challenges [2, 4, 5]. The new tariff rates and silver license rules will continue to be enforced as authorities monitor bullion imports to stabilize the rupee.