Asian currencies including the South Korean won, Indian rupee, Philippine peso, and Indonesian rupiah are under heavy depreciation pressure due to high oil prices, foreign capital outflows, and a strong US dollar [1, 2, 3, 4, 5]. The Indonesian rupiah breached the 18,000 per US dollar level, the South Korean won hit its weakest since the 2008 financial crisis, and the Indian rupee and Philippine peso reached record lows [1, 3, 4, 5].

South Korea's finance ministry announced plans on June 7 and reiterated them on June 11 to strengthen oversight of offshore currency derivatives and to extend trading hours while allowing overseas investors to trade onshore forex markets [1, 2, 3, 4, 5]. India tightened banks' net open foreign exchange position limits to $100 million USD to reduce speculative activity [1, 2, 3, 4, 5]. The Philippines government instructed banks to restrict non-deliverable forward (NDF) contracts to genuine economic reasons [1, 2, 3, 4, 5]. Indonesia's central bank raised interest rates unexpectedly on June 9 and said it is continuously intervening around the clock in currency markets to support the rupiah [1, 3, 4, 5].

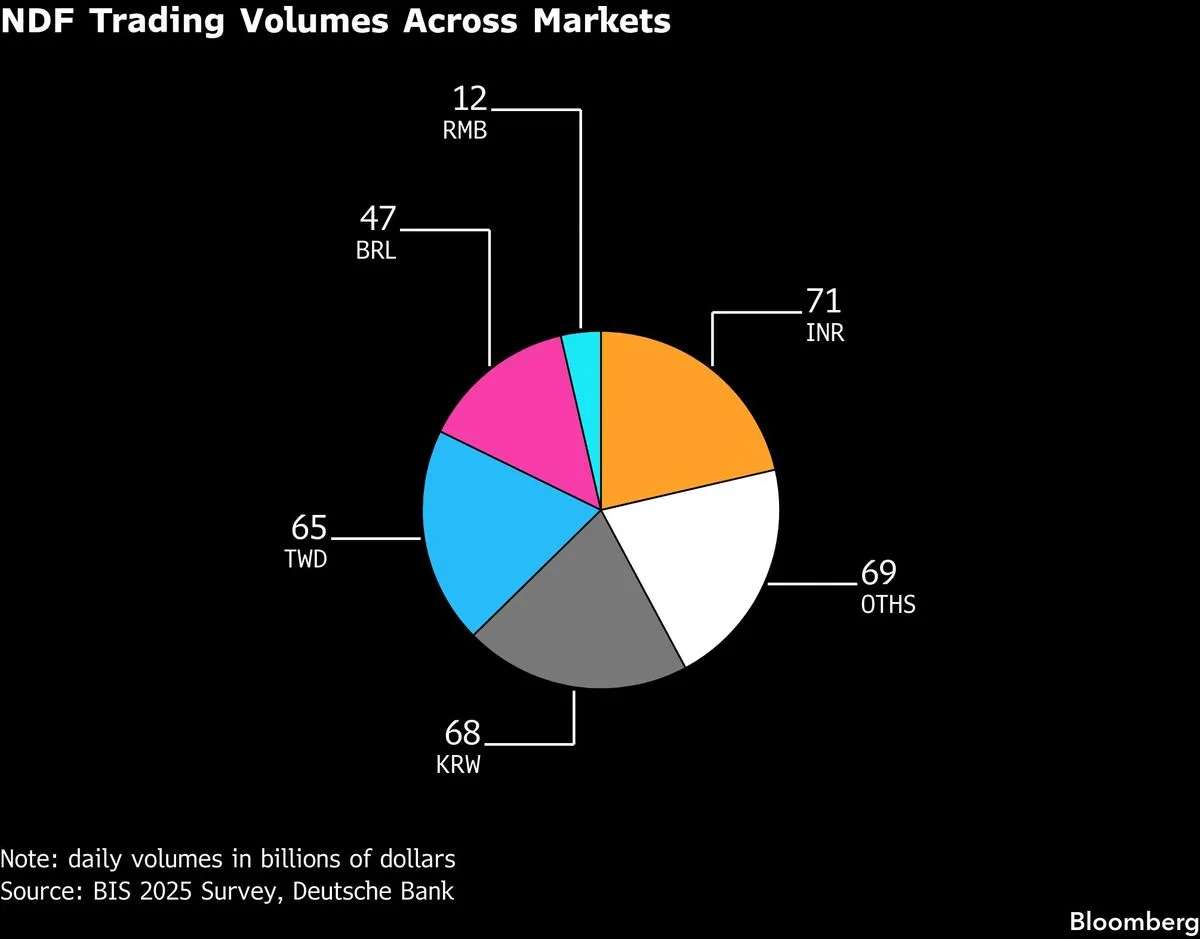

NDFs, which account for about 4% of the $10 trillion daily global FX market, play an outsized role in Asia because onshore currency convertibility remains limited [1, 3, 4, 5]. Indian central bank offshore USD short positions linked to derivatives may have risen to around $115 billion USD as part of efforts to defend the rupee [3]. Large foreign capital outflows have weighed heavily on local currencies, with India facing $30 billion USD in net foreign portfolio sell-offs and South Korea suffering over $78 billion USD in net foreign sell-offs so far in 2026 [3, 4, 5].

Some investors point to domestic economic issues as the main driver of currency weakness rather than offshore speculation [3, 4, 5]. Michael Wan, senior currency analyst at MUFG Bank, said, "It may have some impact, but ultimately for the measure to be successful there needs to be a shift in the fundamentals as well" [1]. ANZ Asia Research Head Khoon Goh noted the demand for NDFs stems from restrictions in domestic markets and expects that easing these would reduce offshore trading interest [3].

OCBC Senior Economist Lavanya Venkateswaran said central banks' interventions aim to prevent more volatile market swings and indicated further interest rate hikes are possible in India, the Philippines, and Indonesia [4, 5]. The coordinated regulatory tightening and market interventions follow heavy foreign capital outflows and widespread currency depreciation across Asia in 2026 [3, 4, 5].